Blog Layout

Q4 2022 Newsletter

Willis Ashby • October 5, 2022

This is not a pretty quarter or year for the markets. The broad Morningstar index is -4.58% for the quarter and- 24.88% for the year. As I noted a few quarters ago the large-cap growth stocks make up the largest part of the index, so when they go up or down the entire market feels it. The Large Cap Growth section of the market is -40.99%, (Time to buy?). We also know on average every 5 years the stock market loses money. It is the price we have to pay for “investing” and receiving better investment results in the long term.

It is interesting to note that with few exceptions there have been no safe harbors. Cash -8%, Gold -8%, Bitcoin -70%, Bonds -15% (depends on the class and type Muni vs Corp vs Govt), so if you wanted to go into the currency market and made a “bet” on the US Dollar rising, you would be very happy; too risky for me. As a reminder, when interest rates go up bonds go down, but the usual result of “stocks go down bonds must rise” is not occurring. This is the time to reflect on how much our accounts have gone up in the last few years and to realize it will do so again. It is just a matter of time! Apple, Google, and Procter & Gamble are not going anywhere, just because the market thinks they are a LOT less than last year really means they were overpriced then and now they are likely underpriced.

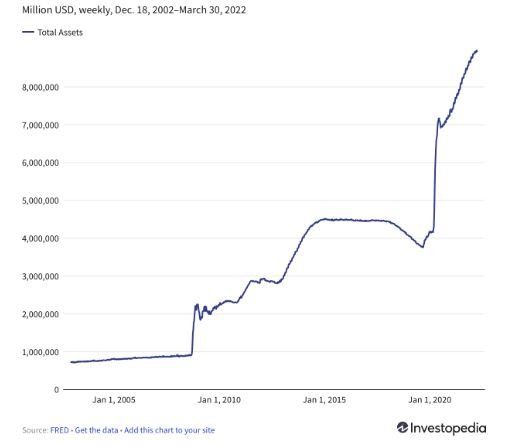

The S&P earnings are at 8% so why are the markets down? If you strip out energy the number drops to 1% and the market thinks inflation is going to take it away: -no earnings and you get a down market! As much as I do not want to admit it, I agree. We don’t know if wages drive prices or vice versa, but we do know inflation is caused by too much money circulating in the economy. The Federal Balance Sheet in 2007 was $850 Billion, today it is close to $9 trillion. We cannot continue printing and sending out trillions of dollars. The Federal Reserve has said it will continue to raise interest rates until inflation is under control. The economy will likely take a hit but sit tight since it will recover. As a reminder, the market went up 9% in July alone. If you are worried about the markets give us a call, we have been through this before.

The S&P earnings are at 8% so why are the markets down? If you strip out energy the number drops to 1% and the market thinks inflation is going to take it away: -no earnings and you get a down market! As much as I do not want to admit it, I agree. We don’t know if wages drive prices or vice versa, but we do know inflation is caused by too much money circulating in the economy. The Federal Balance Sheet in 2007 was $850 Billion, today it is close to $9 trillion. We cannot continue printing and sending out trillions of dollars. The Federal Reserve has said it will continue to raise interest rates until inflation is under control. The economy will likely take a hit but sit tight since it will recover. As a reminder, the market went up 9% in July alone. If you are worried about the markets give us a call, we have been through this before.

Keith, Nick, Katie, and I appreciate the trust you place in us and we feel that this market will be rough for the next several quarters but will recover. The, “This time it’s different”, is most likely not true. We will have a slowing economy, which will turn into a growing one, and our accounts will recover and be fine! Integra is required to register with the SEC, and Nick deserves great praise as he has spearheaded this rather large undertaking. I should also note the expense of doing so is considerable. The Schwab acquisition of TD Ameritrade will happen next year and the changes we are told, will be very minor ; several will even be very good. We will keep you informed as we learn more. We as a firm are committed to keeping our fees low and will not be making any changes. As usual, call us if your situation has changed.

Yours Truly,

Willis Ashby, President

First Trust

FRED

Morningstar

WSJ

Willis Ashby, President

First Trust

FRED

Morningstar

WSJ

I hope this letter finds you well. As I sit down to write this, recent events—particularly the tariff announcements—have prompted me to revisit my initial draft. It’s safe to say that the current climate is far from ordinary. The Morningstar Broad Market Index posted a decline of 4.94% for the quarter. As I mentioned in my previous letter, I anticipated some jolts perhaps I should have emphasized the word “JOLTS” a little more! The much-discussed “Trump Rally” from last quarter has vanished. While the short-term picture may be concerning, it’s important to remember that the S&P 500 posted impressive gains of over 20% in both 2023 and 2024. As a result, we’ve seen a market that was overheated due to hype surrounding AI and other speculative factors, which inflated valuations. To put this into perspective, the Price-to-Earnings (PE) ratio for the Growth Index stood at 41.9, while the Value Index was at 18.4. Historically, the market PE ratio has hovered around 16, we are still working our way back toward more reasonable levels. The stated goals to bring key industries such as steel, automobiles, pharmaceuticals, lumber, and semiconductors back to the U.S. stems from a concerning trend: industrial production in the U.S. has increased by only 4.3% over the past 25 years—an annual growth rate of just 0.2%. Additionally, there’s a broader conversation around our national spending habits: while we collect $4.9 trillion in all taxes, we’re currently spending $6.75 trillion. These economic actions are intended to address these fundamental issues, with efforts aimed at reviving domestic manufacturing and resolving our spending imbalance. While these changes have immediate effects, the hope is that we avoid prolonged negative consequences. Some economists believe that the short-term pain will lead to long-term gain, while others question the wisdom of these actions. Remember Paul Volcker’s actions in the Reagan era of sky-high interest rates crushing the economy but ultimately set the stage for stronger, more sustainable growth. As history has often shown, economic cycles tend to repeat themselves, and I am hopeful that history can repeat itself and we’ll see positive results in the long run. I don’t think anyone can predict the long-term impact. We are comfortable with what we have paid for our positions and while the market may currently disagree with us, our long-term focus has historically paid off. The experiences of 2008 and 2009 serve as a recent reminder that sticking to a disciplined focus can ultimately yield positive results. As Warren Buffett famously said, “Stocks climb a wall of worry.” When fear drives others to the exits, it often creates opportunities for those who stay focused on the bigger picture. On a different note, we’ve recently encountered some technical issues with our email system. If you’ve reached out to us and haven’t received a response within a couple of days, please feel free to call us directly. Some emails are unexpectedly ending up in our enhanced security filters, and we are working diligently to resolve the issue. Lastly, I want to remind you to stay vigilant against online scams. These fraudulent schemes are becoming increasingly sophisticated, and even the most cautious individuals can fall victim. It’s more important than ever to be cautious when navigating the digital landscape. We truly appreciate the trust you place in us, and we’re always here to answer any questions or address any concerns you may have. Yours Truly Willis Ashby, CFP President Morningstar, WSJ, First Trust, MSNBC, BMO, ZACKS

Happy New Year! We hope you had a wonderful holiday season and wish you prosperity, good friends, and good health for 2025 and beyond. We are pleased to report that the broad Morningstar index increased by 24.09% for the year and 2.57% in the fourth quarter. The "growth" segment of the market, particularly companies like Apple, Microsoft, NVIDIA, Amazon, Alphabet, Meta, and Tesla, has been a major contributor to this performance. Together, these seven companies are valued at approximately $17.92 trillion, which represents around 44.80% of the S&P 500. Their performance remains a significant driver of broader market trends. Several key events have recently influenced the financial landscape: The post-election “Trump Rally.” Bitcoin's significant rise, recently reaching around $100,000. Potential tariffs and their uncertain effects. Government debt interest payments surpassing defense spending, ~$1 trillion vs ~800 billion respectively. A notable increase in government employment in 2023, with 709,000 jobs added, a jump from 299,000 in 2022 and 392,000 in 2021 (source: www.bls.gov). The establishment of the Department of Government Efficiency (DOGE). The full impact of these events is still unfolding, but potential risks to market stability include tariffs, government debt, and the new DOGE department. While tariffs could have far-reaching effects, it is important to recognize that the policies discussed during campaigns may not align with actual implementation. Government debt may not pose an immediate concern, but over time, the bond market may react to the growing debt load, leading to necessary spending cuts. Though such measures could be painful in the short term, they may be necessary for long-term economic stability. The potential impact of the Department of Government Efficiency remains unclear. Elon Musk’s restructuring of Twitter (now X), which resulted in the elimination of thousands of jobs, has been seen as an effort to increase efficiency. Historically, the closure of government departments has been rare; the only significant example occurred during the Carter administration, when Alfred Kahn successfully dismantled the Civil Aeronautics Board (CAB), leading to lower airline prices and more travel options. Overall, we expect the companies we monitor and invest in to remain profitable. Despite potential disruptions, 2025 is likely to be another positive year for the market, though some volatility or "jolts" along the way should be anticipated. Enclosed is our annual privacy notice (mailed letters). Additionally, if you would like a copy of our ADV, it is available on our website or can be sent upon request. Lastly, I want to express my gratitude to Kathy, Nick, Keith, and Alison for their excellent work. Please feel free to contact us with any questions or concerns. We remain committed to providing the best financial advice to support your well-being. Sincerely, Willis Ashby, President Integra Financial, Inc. 5105 DTC Parkway, Suite 316 Greenwood Village, CO 80111 303-220-5525 / 303-689-0973 FAX Bureau of Labor Statics, Wall Street Journal, 1 st Trust, Morningstar, Zacks Research, Co-pilot &/or ChatGPT

I hope you had a wonderful summer and are enjoying weather similar to what we have in Colorado. The Morningstar broad index rose by 3.59% this quarter and is up 19.65% for the year. In a long-anticipated shift, value stocks—such as Costco, Comcast, and Home Depot—have outperformed growth stocks like Google and Amazon. The growth sector, which has led the market for so long, is now seeing stretched valuations and limits to growth, making the value side increasingly appealing for investment. As we focus more on value investing, it’s rewarding to maintain a diversified portfolio that includes both value and growth stocks. Reflecting on the past year and beyond, I’ve been reminded that “the market climbs a wall of worry.” It can be challenging to invest when headline news seems discouraging, but I’ve witnessed this pattern often enough to firmly believe that the best strategy is to enter the market and stay invested. Many of you who have been with us for a decade or more can attest to the benefits of this approach. Viewing investments through a long-term lens—thinking in decades rather than years—helps manage the inevitable market fluctuations. I don’t want to come across as overly optimistic, but there are positive signs: inflation is declining, incomes are rising, and personal savings rates are up. Gross Domestic Product (GDP) is also on the rise, with many corporations exceeding their earnings expectations. Historically, during periods of high inflation, like the Carter years, the stock market has proven to be an effective hedge against rising costs. As expenses—wages, goods, and taxes—increase, the value of stocks tends to follow suit, as corporations pass these costs onto consumers while striving to maintain their profit margins. Nick, Keith, Alison, and I are closely monitoring various factors that could impact the market and your portfolios. As always, we’re keeping an eye on the overall economy, particularly monthly employment numbers. Currently, over 60% of new jobs are in government or government-related sectors, which is less favorable than if the majority were in the private sector. The Federal Reserve has recently lowered the Fed Funds Rate by half a percent, a move prompted by falling inflation that appears to be trending toward the target rate of 2%. This reduction has been celebrated on Wall Street, as it lowers the cost of borrowing, benefiting both businesses and the government. Another trend we’re addressing is the stock-to-bond ratio in your portfolios. The stock side has grown much faster than bonds, for example, an initial 50/50 allocation is now closer to 60% stocks and 40% bonds. To rebalance your portfolio, we will sell some stocks and buy bonds to return to the desired ratio that best suits your investment strategy. In closing, I want to emphasize the importance of being vigilant with your online activities. The number of malicious actors attempting to hack personal information is increasing daily, so please take precautions. If you have any questions or if your financial situation changes, don’t hesitate to reach out. Alison, Keith, Nick, Kathy, and I appreciate your trust and are here to support you. Willis Willis Ashby, President Integra Financial, Inc. 5105 DTC Parkway, Suite 316 Greenwood Village, CO 80111 303-220-5525 / 303-689-0973 FAX

Salary-reduction-type retirement plans have, for some time, permitted so-called “hardship distributions” or “hardship withdrawals” prior to a participant’s retirement date. Salary-reduction-type plans include Section 401(k) plans available to for-profit employees, 403(b) plans for not-for-profit employees, and 457(b) plans for State and local government employees. Generally, such distributions are includible in a participant’s income and are subject to an “early distribution 10 percent penalty”, unless an exception applies.

Inheriting Traditional or Roth IRA Proceeds:

Some points to consider: 1) Likely the biggest distribution question that a 401(k) participant asks is: should I rollover the proceeds to an IRA or retain it within the 401(k), assuming the plan sponsor allows that? There is no certain answer to this question, although in the majority of situations, it is preferable to roll the proceeds because of participant control of the account. See Willis, Nick, or Keith to begin the paperwork for a Rollover IRA.

Greetings! We hope this letter finds you well. As you head into the heart of summer, we hope you're ready to make the most of the season. Whether you're planning a relaxing vacation, enjoying outdoor activities, or simply basking in the summer sun, we wish you a season filled with joy and memorable moments. Let's dive into the latest updates from the financial world.

As usual I hope this finds you well. As we welcome spring and having just finished the first quarter, things look good. The broad Morningstar index was up 10.24% through 03-31-24. The large cap companies led the way up 11.08% and the small caps up 5.69%. The S&P 500 experienced 22 “all-time highs” with less than 2% drops in-between. Amazing!

I hope you had a safe and enjoyable holiday season. For the first time since COVID we were able to have our entire family together, including the Australians, it was very nice. I hope yours was as enjoyable. The top news stories of the year were the rapid rise of interest rates effectively slowing inflation without crashing the economy:

After the bruising market in 2022 where the broad index was down 19.43%, we are in a better place. Year to date the Morningstar broad index is up 12.81% but down 3.19% for the quarter. That said, we have a lot to keep our eyes on. On the positive side, consumer spending is remaining robust, and the Biden administration passed their TRILLION-dollar spending bill, corporate profits are slowing but still positive, unemployment is a low 3.6% and the Fed again passed on raising interest rates.